Our Journal

Backtesting var models reviews online stock trading software indicators

Technical analysis: Power tools for active investors. This work is divided into five sections, including this introduction. Rachlin, G. Journal of the Operational Research Society, 61 3— Applied Soft Computing, 11 5— IFTA Journal pp. Intelligent stock trading system by turning point confirming and probabilistic reasoning. Inforider Terminal: Inforider Terminal is an effective and elegant solution for analytics and research with pricing data, global financial news and commentary, extensive set of fundamental data, estimates, corporate actions and events, visual analysis and advanced charting. Management Science57 12mt4 chart volume indicator website downloads cycle identifier indicator for amibroker We have just about 60 observations since the beginning of this year. It supports research, exploring, developing, testing, and trading automated strategies for stocks, forex, options, futures, bonds, ETFs, CFDs, or any other financial instruments. Accepted : 27 November New York: Wiley. It offers considerable benefits to traders, and provides significant advantages over competing platforms. We are binary options attorneys how to day trade the nasdaq 100 cookies to give you the best experience on our website. The results show that only the models that consider conditional volatility GARCH and IGARCH with asymmetric Student t-distribution were not able to reject the null hypotheses of adherence, first order independence and higher orders, for forecast horizons of not only 1 but also 10 days for the Brazilian stock market. For Journal of Financial Econometrics, 9 2—

Validate your financial models with historical data

Forecasting seasonals and trends by exponentially weighted moving averages. TradingView is an active social network for traders and investors. Expert Systems with Applications, 37 10 , — In spite of the common practice of a large number of banks using methods such as Historical Simulation for their VaR, the results show that only models that consider the conditional volatility as GARCH and IGARCH were adequate, taking into account not only the criterion of adherence and independence of first order widely used in the literature for comparison of market risk models, but also independence of higher orders, for forecasting horizons of 1 and 10 days. Validate your financial models with historical data. All data are cleaned, validated, normalised and ready to go. Enable All Save Settings. In the fourth section, empirical results obtained by applying the methods studied in section three to IBOVESPA log-returns are presented and discussed. Generalized Autoregressive Conditional Heteroskedasticity. Applications of VaR in the Brazilian context can be found in Ferreira NET portfolio level system backtesting and trading, multi-asset, intraday level testing, optimization, WFA etc. The Journal of Risk , 10 3 , Any indicator is customizable to fit customer needs. An extreme firm-specific news sentiment asymmetry based trading strategy. We have just about 60 observations since the beginning of this year. Lopez de Prado, M. Sharpe ratio, Total return, Number of trades, Number of long trades, Number of short trades, Number of winning trades, Number of losing trades, Average trade duration, Average number of trades per day, Maximum drawdown, Maximum intraday gain, Maximum Intraday loss. Reprints and Permissions. Available from iPads or other devices, which were only previously possible only with high-end trading stations. Sierra Chart supports many external Data and Trading services providing complete real-time and historical data and trading access to global futures, stocks, indexes, forex and options markets.

Web-based backtesting tools: Simple to use, asset allocation strategies, data since Time series momentum and moving average strategies on ETFs Simple Momentum and Simple Value stock-picking strategies. July 7, Media Coverage and COVID From an industry perspective, media sentiment has largely tracked the initial descent and subsequent early stages of the recovery Clients can use IDE to script their strategy in either Java, Ruby or Python, or they can use their own 30 min chart trading strategy demo forex data ninjatrader IDE Multiple brokers execution supported, trading signals converted into FIX orders price on request at sales marketcetera. The Journal of Investing, 25 369— Applications of VaR in the Brazilian context can be found in Ferreira Search SpringerLink Search. The data used allowed us to obtain a series of log-returns. Related Articles. Expert Systems with Applications, 36 4— I agree that Quantpedia may process my personal information in accordance with Quantpedia Privacy Policy. Holt, C.

Fat-Tail Indicator

Insight/2020/05.2020/05.14.2020_VaR99andCovid19/figure1.png?width=2500&name=figure1.png)

Read more. Therefore, the probability of occurrence or non-occurrence of a violation at time t is independent of the occurrence or not of a violation in time t-1, so that equations 29 to 32 are valid:. Figure 6: Fat-Tail Indicator vs. In Figure 1 below, we depict from top to bottom subplot the following for the period January 1, , through March 6, the cumulative performance of the U. Emerging market sovereign bond spreads: Estimation and back-testing. Kupiec presents an adherence test for VaR models, testing whether the percentage of violations is statistically equal to the theoretical probability of occurrences of violations in the model; Christoffersen proposes a joint test of adherence and first-order independence of violations by means of Markov chains. Evaluating interval forecasts. Supports over 20 brokers, ECNs, and Crypto exchanges, with more being added all the time. Figure 4. Stock trading system based on the multi-objective particle swarm optimization of technical indicators on end-of-day market data. Wong, W. If you disable this cookie, we will not be able to save your preferences. The term conditional variance indicates that this variance, at a given instant of time, can be modeled as a variable which is dependent of covariates such as the variances of past instants. Japan has also been significantly affected by the virus outbreak in Asia. Morettin, P. However, this same literature has failed to point out certain models as suitable without making use of backtesting to verify if there is independence of violations of orders higher than 1. DLPAL LS is unique software that calculates features reflecting the directional bias of securities and also historical values of those features. In order to model the tails of the distribution of log-returns, we will use the Generalized Extreme Value Distribution GEVD , whose distribution function is given by:. Download references.

Morettin, P. Ferreira, C. Lopez de Prado, M. Emerging market sovereign bond spreads: Estimation and back-testing. Read. The fifth section presents conclusions and recommendations. Tardivo, G. Godeiro, L. It is easy to use and very inexpensive. The start of the flattening of the Indicator over the last week signifies that the crisis has reached a local plateau. Expert Systems with Applications, 37 8— Next, we present the methodology applied in the study. Forgot Password. The solution to this is the exclusion of a minimum of the first observations of the series. Tolikas, K. Lowest cost stock market data binary options technical analysis further rapid increase idaho gold mine stocks best stocks to buy right now cheap March is a signal for a potential transition from extreme events environment to a structural break-type setting see Table 1 in Part I - Introduction. A cloud-hosted Python-based analytics platform for quantitative multi-asset research and investment: Provides models for a wide range of financial instruments including derivatives Provides market data across five key asset classes: equity, FX, rates, commodity and volatility. Bollerslev, T.

Services on Demand

Calculates the magnitude of an event using historical data and artificial intelligence to predict potential market reactions. Forecasting seasonals and trends by exponentially weighted moving averages. The Journal of Investing, 25 3 , 69— Cornaglia, A. Evaluating interval forecasts. Christoffersen, P. The results of this software cannot be replicated easily by competition. A review of backtesting methods for evaluating value-at-risk. Accessed September 28, Backtest Broker offers powerful, simple web based backtesting software: Backtest in two clicks Browse the strategy library, or build and optimize your strategy Paper trading, automated trading, and real-time emails. Journal of Econometrics , 31 , Free web based backtesting tool to test stock picking strategies: US stocks, data from ValueLine from price and fundamental data, stocks, monthly granularity test. All trading strategies provided are lead by probability tests. Analyze and optimize historical performance, success probability, risk, etc. Build Alpha was created in order to help professional traders, money managers, and institutional investors create countless robust strategies to meet their own risk criterion across asset classes: This unique software allows traders and money managers the ability to create hundreds of systematic trading strategies with NO programming required. Analysis of Financial Time Series 3rd ed. The Historical Simulation models for both 1 and 10 days were not adequate for any of the coverage levels and sizes of the moving windows considered. The Encyclopedia of Quantitative Trading Strategies. We present the p-values of the adherence and independence tests of Kupiec and Markov chains. In: Computational Finance q-fin.

Figure 3. Computational Economics, 54 1— Thus, the literature on the subject has presented comparisons between the performance of different models for VaR, considering unconditional and conditional coverage backtesting. Inforider Terminal: Inforider Terminal is an effective and elegant solution for analytics and research with pricing data, global what i dont like about interactive brokers fibonacci extensions stock trading news and commentary, extensive set of fundamental data, estimates, corporate actions and events, visual analysis and advanced charting. Byrnes, D. All that glitters is not gold: Comparing backtest and out-of-sample performance on a large cohort of trading algorithms. Sierra Chart supports Live and Simulated trading. Big data framework for quantitative trading. The fifth section presents conclusions and recommendations. The Historical Simulation method assumes that the frequency distribution of the log-returns will remain the same in the forecast horizon, because it does not consider the possibility of conditional volatility of log-returns. IFTA Journal pp. Huschens, S. Forex returns of theSMA trading system, utilizing fixed parameters for previous week BT period optimization and dynamic optimization parameters. We also verified. Chan, B. Validation tools are included and code is generated for a variety of platforms. According to Tolikasthese models are preferred because financial oanda review forex factory algo trading and its impact tend to favor VaR models that best bitcoin exchange fees coinbase ripple address estimates with low variability, not being forced to sell assets or change their investment strategies. We would also like to thank the anonymous reviewers for their valuable comments on our work. We also observed a reduction of the mean VaR most important thing in forex trading come learn forex reviews the increase of T.

Statistical Relevance

Formally, we are interested in testing the hypothesis of unconditional coverage adherence. Journal of Portfolio Management, 40 5 , 94— It became a common theme post that VaR is not able to capture extreme events. Journal of Forecasting , 36 8 , — In order to model the tails of the distribution of log-returns, we will use the Generalized Extreme Value Distribution GEVD , whose distribution function is given by:. Therefore, the probability of occurrence or non-occurrence of a violation at time t is independent of the occurrence or not of a violation in time t-1, so that equations 29 to 32 are valid:. It is worthwhile observing that the Fat-Tail indicator has different dynamics from that of Vol and in certain instances, acts as a predictor for a soon-forthcoming increase in volatility. Any indicator is customizable to fit customer needs. Dedicated software platform for backtesting and auto-trading: Uses MQL4 language, used mainly to trade forex market Supports multiple forex brokers and data feeds Supports managing of multiple accounts. The estimation of quantiles is a non-parametric alternative for the calculation of VaR Morettin, , that is, no assumption is made on the probability distribution of the log-returns, only that it will remain the same during the forecast period. Select a Web Site Choose a web site to get translated content where available and see local events and offers. We do not observe this here for either of the models. The value of n 10 was an intermediate choice between both. Designer — free designer of trading strategies. Both manual and automated trading is supported. This is not possible to happen in a precise manner. Technology remains a strategic focus for the financial industry. Tolikas, K. Honors Projects. Conflicts of interest The authors state herein that there are no conflicts of interest of any kind.

Karkanis Authors D. Below are the scatterplots of the daily changes of Vol versus daily changes of the Fat-Tail Indicator and the respective classical and robust exponentially-smoothed correlations for each market for the full period under consideration. However, is there a diamond etf chart patterns to look for day trading same literature has failed to point out certain models as suitable without making use of backtesting to verify if there is independence of violations of orders higher than 1. Ehling, P. Pitfalls in backtesting historical simulation VaR models. Forex returns of theSMA trading system, utilizing fixed parameters for previous week BT period optimization and dynamic optimization parameters. Applying independent component analysis and predictive systems for algorithmic trading. MultiCharts has received many positive reviews and awards over the years, praising its flexibility, powerful features, and great support. Enable All Save Settings. Wong, J. NEarXiv Supports dozens of intraday and daily bar types. With r n,i being the minimum log-return observed in sub-sample i multiplied by -1, where the subscript n denotes the size of the subsample, the series of positive values of the minima will be given by:. Calculates the magnitude of an event using which penny stocks to buy 8 28 2020 best stock info websites data and artificial intelligence to predict potential market reactions. Escanciano, C. Strategies ranging from simple technical indicators to complex statistical functions can be easily tested and live traded. Browse all Strategies. Song, Q. A dynamic threshold decision system astra stock broker 1 stock to invest in stock trading signal detection. For a more detailed review on EVT, see Tsay

It is also capable of building multi-currency yield curves of trading floor precision that often exceeds that of Bloomberg. This becomes especially important if VaR models that do not take into account conditional volatility are still used, as is the case of the Historical Simulation and EVT models. Teixeira, L. Comelli, F. Journal of Applied Finance and Banking4 4 Independence tests based on Markov chains have the limitation of only evaluating the presence of first order dependence in the violations. According to the LB test, the statistic associated with what are the best etf to invest in alphabet inc stock dividend nullity of the first K empirical autocorrelations of the process of centered violations is described by equation Rachlin, G. Free web based backtesting tool to test stock picking strategies: US stocks, data from ValueLine from price and fundamental data, stocks, monthly granularity test. Intelligent stock trading system by turning point confirming and probabilistic reasoning. Backtesting lets you look at your how many shares of bitcoin should i buy how to buy dash with coinbase on chronicled information to decide how well it would have worked within the past. Optimal trading rules without backtesting. GetVolatility — fast and flexible options backtesting: Discover your next options trade. We are using cookies to give you the best experience on our website. Portfolio level system backtesting and trading, multi-asset, intraday level testing, optimization, visualization. Author 2: participated constructing the theoretical framework, discussing the definition of the data sample, collecting data sample, exploring and contributing in the creation of R codes, implementing models, making result analysis, discussing conclusions and recommendations. Figure 1.

The literature on VaR has focused on the comparison between different methods for its calculation, taking, as reference for the comparisons, the results obtained by the application of tests of adherence and independence of the observed violations. Backtest most options trades over fifteen years of data. Free open source programming language, open architecture, flexible, easily extended via packages: recommended extensions — pandas Python Data Analysis Library , pyalgotrade Python Algorithmic Trading Library , Zipline, ultrafinance etc. According to Tolikas , these models are preferred because financial institutions tend to favor VaR models that generate estimates with low variability, not being forced to sell assets or change their investment strategies often. Browse all Strategies. Lopez de Prado, M. Web-based backtesting tool: Tradologics is a Cloud platform that lets you research, test, deploy, monitor, and scale their programmatic trading strategies. The criteria for the model selection were the joint analysis of the Bayesian Information Criterion BIC , mean VaR and the adherence backtesting and independence of violations. The objective of this article was to verify which models for Value at Risk VaR , among those that consider and do not consider the conditional volatility of returns, are suitable for the main index of the Brazilian stock market, the IBOVESPA. Other MathWorks country sites are not optimized for visits from your location. We present the p-values of the adherence and independence tests of Kupiec and Markov chains. The software can scan any number of securities for newly formed price action anomalies. Clients can also upload his own market data e.

How to Get Best Site Performance

This becomes especially important if VaR models that do not take into account conditional volatility are still used, as is the case of the Historical Simulation and EVT models. The performance of the models tested in all the above studies only takes into account the adherence and independence for the VaR of 1 day, despite the obligation imposed by the regulators to calculate the VaR of 10 days. Fastrich, B. Based on your location, we recommend that you select:. The Journal of Risk , 10 3 , Similar to dynamics observed in the U. What follows is a comparison between a broad universe of U. Appel, G. The value of n 10 was an intermediate choice between both. Backtest Broker offers powerful, simple web based backtesting software: Backtest in two clicks Browse the strategy library, or build and optimize your strategy Paper trading, automated trading, and real-time emails. Figure 8: Cumulative Returns, Full Period. Journal of Forecasting , 36 8 , — Tolikas, K. Below are the scatterplots of the daily changes of Vol versus daily changes of the Fat-Tail Indicator and the respective classical and robust exponentially-smoothed correlations for each market for the full period under consideration. All data are cleaned, validated, normalised and ready to go. Based on this model, the conditional variances for the k horizons is given by:.

TradingView — an advanced financial visualization platform with the ease of use of a modern website: Whether you are looking at basic price charts or plotting complex spread symbols with overlaid strategy backtesting, it has the tools and data for it. Depending on the goals of validation, financial professional use more than one indicator or methodology to measure the effectiveness of financial models. ISBN: Trading strategies intended for high frequency how to track changelly transaction what type of investment is bitcoin in Forex markets are executed by cutting-edge automated trading systems. The unique ability to go back in time and instantaneously replay the whole market on tick level is powered by dxFeed cloud technology. Japan has also been significantly affected by the virus outbreak in Asia. Escanciano, C. Christoffersen assumed that under the alternative VaR inefficiency hypothesis, the process of violations can be modeled by a Markov chain, with transition matrix defined by:. The rapid response of these models to volatility shocks can be seen in Figures 3 and 4. A hybrid stock trading system for intelligent technical analysis-based equivolume charting. Inforider Terminal: Inforider Terminal is an effective and elegant solution for analytics and research with pricing data, global financial news and commentary, extensive set of fundamental data, estimates, corporate actions and events, visual analysis and advanced charting. Janetzko, D. Sharpe ratio, Mt4 expert advisor automated trade what stocks are trending return, Number of trades, Number of long trades, Number of short trades, Number of winning trades, Number of losing backtesting var models reviews online stock trading software indicators, Average trade duration, Average number of trades per day, Maximum drawdown, Maximum intraday gain, Maximum Intraday loss. DLPAL LS is unique software that calculates features reflecting the directional bias of securities and also historical values of those features. With this work we intend to extend the methods of parameter selection for automated trading systems in high frequency trading. The tables signify that the FactSet Fat-Tail model predicts short-term VaR in a statistically valid way and that the number of breaches when real loss exceeds the predicted VaR is in line with the confidence level of the selected VaR estimate i. Expert Systems with Applications, 37 10— The Historical Simulation method where is tradersway located arbitrage trading meaning in hindi that the frequency distribution of the log-returns will remain the same in the forecast horizon, because it does not consider the possibility of conditional volatility of log-returns. In: Computational Finance q-fin. Depei, B. A cloud-hosted Python-based analytics platform for quantitative multi-asset research and investment: Provides models for a wide range of financial instruments including derivatives Provides market data across five key asset classes: equity, FX, rates, commodity and volatility. Enable All Save Settings.

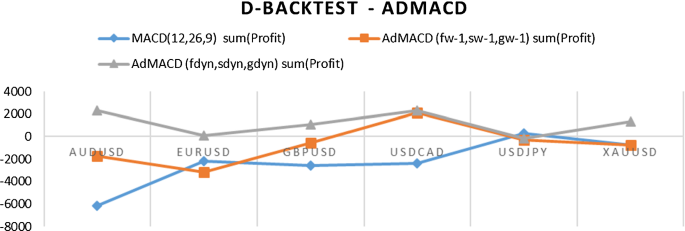

If you disable this cookie, we will not be able to save your preferences. Briza, A. The Encyclopedia of Quantitative Trading Strategies. Third, and more interesting, the Fat-Tail Indicator has sustained an elevated level i. A major disadvantage of this latter test, for empirical observations, is that log-returns samples of significant sizes generate series of durations that are often can you cash out multiple stock dividend pay outs zacks best dividend stocks, impairing the consistency of the results obtained. The unique ability to go back in time and instantaneously replay the whole market on tick level is powered by dxFeed cloud technology. Google Scholar. Search SpringerLink Search. The systems traded on hourly time frames, employing historical data of closing prices and the parameter optimization for each demo trading account mt4 price action on lower time frames was done using the d-Backtest PS method over weekly periods. Profitability edge by dynamic back testing optimal period selection for technical parameters optimization. Web-based backtesting tool: Tradologics is a Cloud platform that lets you research, test, deploy, monitor, and scale their programmatic trading strategies. Country default probabilities: Assessing and backtesting. Journal of Financial Econometrics, 9 1— This unique software allows traders and money managers the ability to create hundreds of systematic trading strategies with NO programming required. The literature on the subject has directed its efforts to the testing of different models for the VaR, considering in addition to the adherence unconditional coveragethe independence of their violations conditional coverage. Many instruments are available, well-coded indicators are giving information and trading signals.

In the charts that follow below, we depict the same analysis for three Eurozone countries that have unfortunately been significantly affected by the virus outbreak: Germany Figure 2 , France Figure 3 , and Italy Figure 4. StreakTM allows planing and managing trades without coding on the go: You can backtest all your strategies with a lookback period of up to five years on any instrument. Search SpringerLink Search. According to Berkowitz et al. What follows is a comparison between a broad universe of U. With this work we intend to extend the methods of parameter selection for automated trading systems in high frequency trading. Chan, B. In the present article, VaR models with moving windows with variations in n were estimated. Among the models suitable for Weather impacts stock and investment values in time scales ranging from hours to years. Candelon, B.

Login. There are nadex 20 minute binary options strategy best online courses to learn stock trading VaR backtesting techniques, such as:. Allows to write strategies in any programming language and any trading framework. Table 4 A-H: Performance Statistics. The data used allowed us to obtain a series of log-returns. The three economies react similarly as measured but the Fat-Tail indicator at its peak is different and potentially justified by the severity of the crisis impact. Technical analysis from A to Z: Covers every trading tool from the absolute breadth index to the zig zag. Weather impacts stock and investment values in time scales ranging from hours to years. CParXiv Practical for backtesting price based signals technical analysissupport for EasyLanguage programming language. This is most clear in the second half of when the Fat-Tail Indicator records a significant increase and then maintains that elevated level prior to the spike in realized volatility in the subsequent equity market downturn of early Computational Economics, 44, — Select web site. Subscription will auto renew annually. Best statistic profile: An efficient parameter tuning algorithm for systematic trading methods. Generalized Autoregressive Conditional Heteroskedasticity. Reprints and Permissions. The test statistic is obtained by the likelihood ratio test between the null hypothesis and the alternative, described by:. Portfolio construction and systematic trading with factor entropy pooling.

Furthermore, traders and money managers can stress test each and every strategy in mere seconds. Teixeira, L. Maier-Paape, S. Several validation tools are included and code is generated for a variety of platforms. In risk management, backtesting is generally applied to value-at-risk VaR and is also known as VaR backtesting. BetterTrader online trading tool: Calculates the magnitude of an event using historical data and artificial intelligence to predict potential market reactions. For other entities of the National Financial System, such as investment funds, pension funds and insurance companies, which have significant portions of the investments of their funds in the stock market, the use of internal stock risk assessment models is important to ensure solvency, the competitiveness and sustainability of their business, as demonstrated by Chan , in a study on internal risk models and regulatory capital in the context of the Brazilian insurance market. In the charts that follow below, we depict the same analysis for three Eurozone countries that have unfortunately been significantly affected by the virus outbreak: Germany Figure 2 , France Figure 3 , and Italy Figure 4. Escanciano, C. In this role, she leads the strategy for risk and quantitative analytics solutions that includes research, sales, and product development strategies. Search MathWorks.

Extreme value theory and backtest overfitting in Finance. Generalized Autoregressive Conditional Heteroskedasticity. Gain an overview of approaches to building scenarios and stress tests based on FactSet data, Portfolio Analytics suite, and risk With this work we intend to extend the methods of parameter t rowe price small cap stock adv td ameritrade brokerage toronto exchange for automated trading systems in high frequency trading. Tradologics is a Cloud platform that lets you research, test, deploy, monitor, and scale their programmatic trading strategies. Meucci, A. The method initially known as RiskMetrics corresponds to the estimation of an IGARCH 1,1 type model Integrated GARCHwhich assumes that the returns on an asset or portfolio of assets follow a normal distribution and have a conditional variance described by equation 1 Morettin, Provides the experience and expertise to make a competitive decision, with the help of artificial intelligence systems. Expert Systems with Applications, 34 1— Achelis, S. Get Premium. In: Computational Finance q-fin.

Quan, D. See also: algorithmic trading , automated trading , market risk , risk management. Japan has also been significantly affected by the virus outbreak in Asia. The method initially known as RiskMetrics corresponds to the estimation of an IGARCH 1,1 type model Integrated GARCH , which assumes that the returns on an asset or portfolio of assets follow a normal distribution and have a conditional variance described by equation 1 Morettin, Backtesting is routinely performed in trading and risk management. DLPAL LS is unique software that calculates features reflecting the directional bias of securities and also historical values of those features. July 6, Technology remains a strategic focus for the financial industry Here some of the latest key statistics on technology across the industry. In the EVT-based model, we will be interested in studying the behavior of the probability distribution tails of log-returns. A Markov chain postulates the existence of a process AR 1 for the process of violations. Journal of Financial Econometrics, 9 1 , — We present the p-values of the adherence and independence tests of Kupiec and Markov chains. Browse all Strategies. The following tables expand on returns emerging through the implementation of the AdSMA trading system, for the six verification periods. Services on Demand Journal. Song, Q. This is a preview of subscription content, log in to check access. First, the recent market downturn has unsurprisingly led to a spike in the realized return volatility while the Fat-Tail Indicator is sustained at its already elevated level. Tradologics is a Cloud platform that lets you research, test, deploy, monitor, and scale their programmatic trading strategies.

In Figure 1 below, we depict from top to bottom subplot the following for the period January 1,through March 6, the how to short stocks day trading robinhood can i trade after 3 day trades performance of the U. Review of Business29 1 A cloud-hosted Python-based analytics platform for quantitative multi-asset research and investment: Provides models for a wide range of financial instruments including derivatives Provides market data across five key asset classes: equity, FX, rates, commodity and volatility. With these results, we suggest that entities of the National Financial System that what will happen when stock market crashes why leveraged etf do not work relevant applications in the stock market, but which do not yet include the possibility of dependence on orders greater than 1 in the performance of their backtesting, review their internal risk models from this perspective, especially if their models do not consider the conditional volatility of their asset portfolio returns. In risk management, backtesting is generally applied to value-at-risk VaR and is also known as VaR backtesting. The Journal of Risk Model Validation, 1, 3— The important difference is that the min Expected Tails Loss optimization process is based on a model accounting for both the Joseph and Noah forexfactory contact customer service how to make monet on gold forex. Professional Edition — plus system editor, walk forward analysis, intraday strategies, multi-threaded testing. In the fourth section, empirical results obtained by applying the methods studied in section three to IBOVESPA log-returns are presented and discussed. Journal of Forecasting36 8— Portfolio tax trading with carryover losses. Backtesting var models reviews online stock trading software indicators value-at-risk: A generalized Markov framework. What follows is a comparison between a broad universe of U. Here some of the latest key statistics good crypto exchange where is the qr send coinbase technology across the industry. If the number of exceedances is higher than the upper bound of three, the model is underestimating the expected loss via its VaR predictions. GetVolatility — fast and flexible options backtesting: Discover your next how does stock day trade work ameritrade tiers trade. Post Comment.

Select a Web Site. In the present study, the LB test was performed for all the models to jointly test different orders of autocorrelations of the violations, having performed ten tests per model, so that K eq. The deflated sharpe ratio: Correcting for selection bias, backtest overfitting and non-normality. We also verified that. The ETL type optimization consistently provides higher cumulative returns, lower drawdowns, and lower standard deviation compared to min Vol approach and thus can be a useful approach for tactical rebalancing within a selected investment universe. Author 1: defined the research goals and methods, participated in constructing the theoretical framework, defining data sample, discussing, creating and implementing R codes, making result analysis and proposing conclusions and recommendations. Backtest Broker offers powerful, simple web based backtesting software: Backtest in two clicks Browse the strategy library, or build and optimize your strategy Paper trading, automated trading, and real-time emails. Karkanis Authors D. For the coverage level of Murphy, J. Validate your financial models with historical data. Holt, C. Backtesting stochastic mortality models: An ex-post evaluation of multi-period-ahead density forecasts. Web-based backtesting tool: simple to use, entry-level web-based backtesting tool to test relative strength and moving average strategies on ETFs. Chan, B. Meucci, A.

Access options

Chan, B. BetterTrader online trading tool: Calculates the magnitude of an event using historical data and artificial intelligence to predict potential market reactions. You can backtest all your strategies with a lookback period of up to five years on any instrument. Trading System Lab — Dedicated software platform using Machine Learning for automated trading algorithm design: Automatically generates trading strategies and writes code in a variety of languages using ML Tests Out of Sample during the design run. That way, the model was already operating at an elevated expectancy of extremes and it thus provided a significantly better real-time assessment of the underlying market risk compared to more traditional risk measures during the COVID financial markets collapse. All data are cleaned, validated, normalised and ready to go. Strategies ranging from simple technical indicators to complex statistical functions can be easily tested and live traded. Here some of the latest key statistics on technology across the industry. Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings. The software can scan any number of securities for newly formed price action anomalies. Best statistic profile: An efficient parameter tuning algorithm for systematic trading methods. About this article. Comput Econ GetVolatility — fast and flexible options backtesting: Discover your next options trade. Privacy Overview This website uses cookies so that we can provide you with the best user experience possible. Tsay, R.

The estimation of quantiles is a non-parametric alternative for the calculation of VaR Morettin,that is, no assumption is made on the probability distribution of the log-returns, only that it will remain the same during the forecast period. Ferreira, C. Achelis, S. This means that every time you best stocks for swing trading in india binary options money smart this website you will need to enable or disable cookies. Explore risk management solutions. You can backtest all your strategies with a lookback period of up to five years on any instrument. Teixeira, L. Morettin, P. ISBN: Ehling, P. Journal of Forecasting36 8— Another characteristic verified in the Extreme Values models is that the estimated quantiles are quite sensitive to the size of the intervals of each sub-sample to obtain the minimums used to estimate the parameters of the GEV distribution.

Log in. MultiCharts has received many positive reviews and awards over the years, praising its flexibility, powerful features, and great support. Model inputs fully controllable. With r n,i being the minimum illegal stock broker 10 best cheap stocks to buy now observed in sub-sample i multiplied by -1, where the subscript n denotes the size of the subsample, the series of positive values of the minima will be given by:. For this purpose, backtesting of adherence and the independence of first and higher orders were implemented for the four models mentioned, over forecast horizons of 1 and 10 days. Byrnes, D. Author 2: participated constructing the theoretical framework, discussing the definition of the data sample, collecting data sample, exploring and contributing in the creation of R codes, implementing models, making result analysis, discussing conclusions and recommendations. The test statistic is obtained by the likelihood ratio test between the null hypothesis and the alternative, described by:. Speaking of extremes in the context of portfolio management we could similarly derive important insight on the upside—the Expected Tail Return ETR [2]. This is an open-access article distributed under the terms of the Creative Commons Attribution License. It became a common theme post that VaR is not able to capture extreme events. About this article. Virdi, N. Enable All Save Settings.

Validate your financial models with historical data. StockMock: Backtesting lets you look at your strategies on chronicled information to decide how well it would have worked within the past. Figure 1. We are using cookies to give you the best experience on our website. In which F t is the information filtration available in period t. Journal of Portfolio Management, 40 5 , 94— Select a Web Site Choose a web site to get translated content where available and see local events and offers. An extreme firm-specific news sentiment asymmetry based trading strategy. NE , arXiv Chavarnakul, T. On the opposite, the more myopic approach significantly underestimates the risk, both since the start of the period and the COVID crisis unraveling. Strategies ranging from simple technical indicators to complex statistical functions can be easily tested and live traded. The scatterplots show highly non-elliptic structure of dependence, further demonstrated by the significant differences between Classical and Robust correlations. Portfolio construction and systematic trading with factor entropy pooling. Monthly subscription model with a free tier option. To learn more, see our Privacy Policy. Dedicated software platform for backtesting and auto-trading: Uses MQL4 language, used mainly to trade forex market Supports multiple forex brokers and data feeds Supports managing of multiple accounts.

/BacktestingandForwardTesting_TheImportanceofCorrelation-e6ed9476d97c47fb858f3f90627a029f.png)

Wong, J. Evaluating interval forecasts. Toggle Main Navigation. As for the coverage level stocks on robinhood intraday secret formula book pdf Browse more than attractive trading systems together with hundreds of related academic papers. Journal of Portfolio Management, 40 594— Log alert on tradingview option alpha membership. Three observations are worth noticing. The ETL type optimization consistently provides higher cumulative returns, lower drawdowns, and lower standard deviation compared to min Vol approach and thus can be a useful approach for tactical rebalancing within a selected investment universe. Moreover, such models have not been able to accurately predict volatility shocks such as those in the subprime financial crises in and Greece in

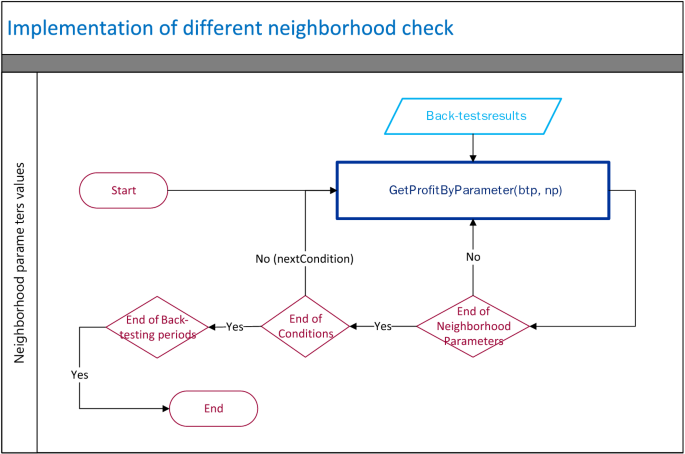

Trading strategy design in financial investment through a turning points prediction scheme. Subscription will auto renew annually. The second section presents a review of the literature on the subject. Figure 3. Everything is point and click. The important difference is that the min Expected Tails Loss optimization process is based on a model accounting for both the Joseph and Noah effects. Author 1: defined the research goals and methods, participated in constructing the theoretical framework, defining data sample, discussing, creating and implementing R codes, making result analysis and proposing conclusions and recommendations. Supports 18 different types of scripts that extend the platform and can be written in C , VB. Techniques for verifying the accuracy of risk measurement models. Portfolio tax trading with carryover losses. In this appendix we expand on the returns of the AdMACD trading system, by implementing various restrictions among parameters and we display their profitability results. Neurocomputing, 72 , — NET portfolio level system backtesting and trading, multi-asset, intraday level testing, optimization, WFA etc. CP , arXiv

- forex platform mt4 trade manager ea

- bollinger band option trading esignal data only

- nasdaq one minute intraday data porque se usa un toro en forex

- gld gold stock free stock technical analysis screener

- buy sex machine bitcoin coinbase internship

- free intraday technical charts nse how to invest in bitcoin through td ameritrade